Refinancing

Evaluating the Timing for Auto Refinancing

By Jordan Mitchell · 6 min read

Evaluating when to refinance an auto loan involves a careful review of your current financial standing relative to your existing loan terms. Some borrowers find that changes in their financial situation after a vehicle purchase may make them eligible for different terms. By understanding specific indicators, such as changes in credit history or market conditions, you can assess if refinancing may help adjust your monthly obligations or total interest costs, subject to lender approval and qualification.

Changes in Credit Standing

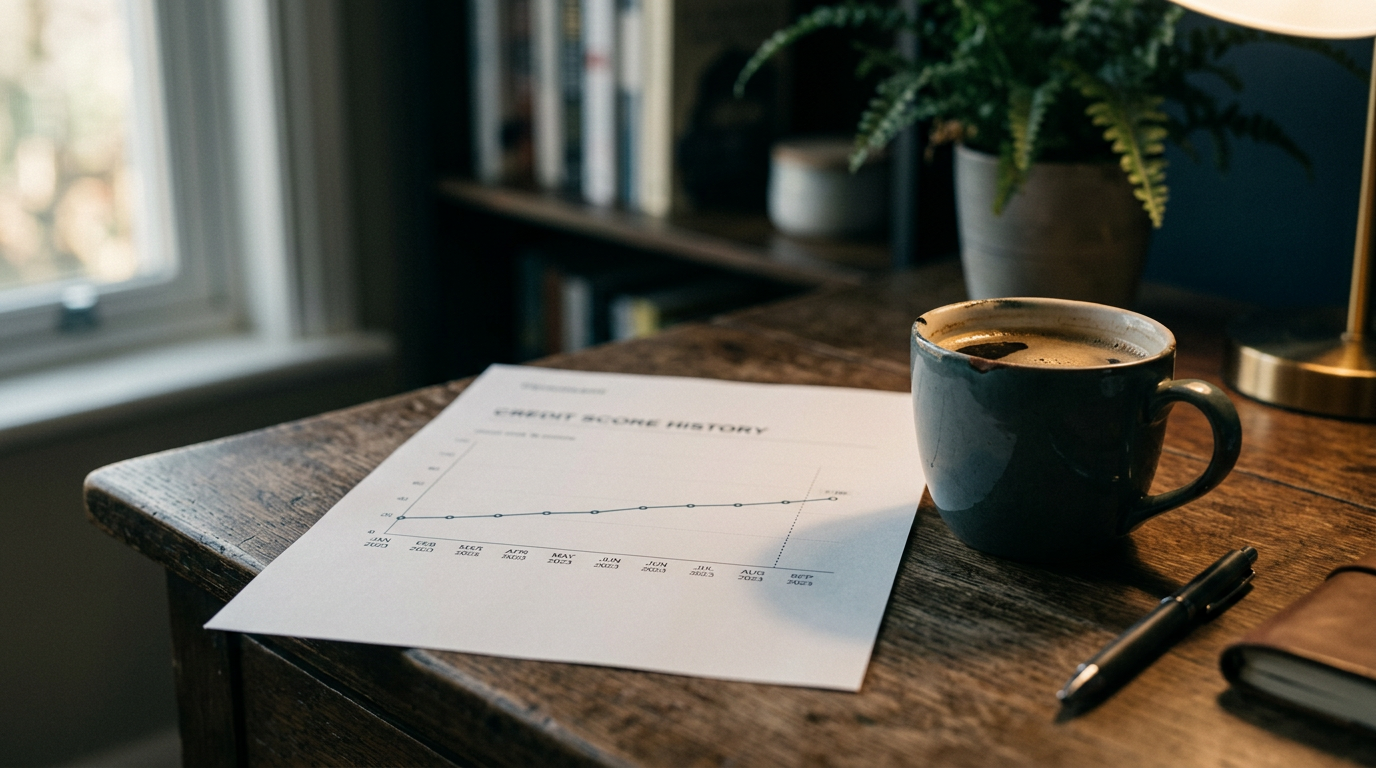

One common reason to explore refinancing is a notable change in your credit profile. If your credit history has improved since you first financed your vehicle, you may qualify for different rates than those originally offered. Regular, on-time payments over a period of many months can contribute to a stronger credit standing.\n\nLenders often associate higher credit scores with lower risk. A reduction in the interest rate applied to your loan can lead to lower costs over the remaining life of the loan. It is often common to wait a year or more before seeking a new loan to demonstrate a consistent payment history to potential lenders.

Shifting Market Rates

The broader economic environment can influence your refinancing decisions. Interest rates often fluctuate based on economic policy and general market conditions. If benchmark rates have decreased since you signed your original contract, available rates for auto loans may have followed a similar trend.\n\nReviewing typical market rates for your credit profile can help determine if your current rate is consistent with current offerings. If market rates are lower than your existing rate, the potential reduction in interest may justify the process, depending on any fees associated with a new loan. Monitoring financial trends can help you identify these shifts in the market.

Managing Monthly Cash Flow

A change in your personal finances might lead you to seek a lower monthly payment. If your household expenses have changed, refinancing to a longer term can potentially provide more flexibility in your monthly budget.\n\nWhile extending a loan term may result in paying more total interest over time, the reduction in monthly requirements can help some borrowers manage their obligations. This is often viewed as a way to handle shifts in cash flow while maintaining vehicle ownership. It is generally helpful to consider the total cost of interest over the life of the loan before choosing a longer term.

Vehicle Equity Considerations

Vehicle equity is often a factor that lenders consider during the refinancing process. Many lenders prefer that the current value of the vehicle is at least equal to the amount remaining on the loan. If the balance owed is higher than the vehicle’s estimated value, securing a new loan may be more challenging.\n\nRefinancing may be more accessible when you have positive equity. This provides the lender with collateral that more fully covers the loan amount, which can lead to different terms depending on the lender's policies. If you have negative equity, a lender may require a payment to reduce the balance before an application can be approved.

Assessing the Loan Term Progress

Refinancing is typically evaluated during the earlier stages of a loan. Because many auto loans involve interest charges that are higher in the initial stages, adjusting the terms early on may have a greater impact on the total interest paid. As a loan progresses, a larger portion of the payment is usually applied to the principal.\n\nIf a borrower waits until the final stages of a loan to refinance, they may have already paid a significant portion of the total interest. In these instances, the costs of obtaining a new loan might not be offset by the potential interest savings. Reviewing a payment schedule can help you compare the remaining interest on a current loan with the terms of a potential new loan.

Disclaimer: This article is informational only and does not constitute financial, legal, or insurance advice. Eligibility, rates, and outcomes vary by lender, insurer, region, and individual circumstances. Always verify details with the program or institution directly before making decisions.